Difference between revisions of "AAA.UncollReins"

(→Two Methods) |

|||

| (6 intermediate revisions by the same user not shown) | |||

| Line 4: | Line 4: | ||

'''Author''': American Academy of Actuaries (AAA) | '''Author''': American Academy of Actuaries (AAA) | ||

| − | [https:// | + | [https://battleacts.discourse.group/c/candidates-6u/aaa-uncoll-reins<span style="font-size: 12px; background-color: lightgrey; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 0px;">'''Forum'''</span>] |

| + | [https://www.battleacts6us.ca/vanillaforum6us/categories/aaa-uncoll-reins '' (Or click here for Legacy Forum – no longer monitored)''</span>] | ||

| + | |||

| + | <span style="display: inline-block; background-color: blue; color: white; font-weight: bold; text-align: center; line-height: 50px; width: 50px; height: 50px; border-radius: 50%;">VIDEO</span> → | ||

| + | [https://battleacts6us.ca/video/230_Uncollectible_Reinsurance_(v01).mp4 <span style="color: black; font-size: 12px; background-color: aqua; border: solid; border-width: 2px; border-radius: 10px; border-color: aqua; padding: 5px 10px 5px 10px; margin-top: 100px;">'''(6:15) → Uncollectible Reinsurance - General Overview'''</span>] | ||

| + | ([[Videos |Click here for all currently available videos.]]) | ||

| + | |||

| + | {| class='wikitable' style='background-color: navajowhite; | ||

| + | |- | ||

| + | || '''BA Quick-Summary''': <span style="color: green;>'''Estimating Uncollectible Reinsurance'''</span> | ||

| + | |||

| + | * The document outlines new GAAP requirements for estimating the uncollectible reinsurance reserve (URR) for property/casualty (P&C) companies under ASU 2016-13. The new rules, effective in 2020 for public companies and 2021 for others, require the URR to be '''based on expected ultimate uncollectible amounts due to credit risk''', which may necessitate new reserving practices for some insurers. | ||

| + | * The document also discusses the importance of reinsurance collectability in evaluating a company's solvency and the various methodologies for estimating the URR, including rating-based and experience-based methods. | ||

| + | |||

| + | |} | ||

==Pop Quiz== | ==Pop Quiz== | ||

| + | |||

| + | [https://battleacts6us.ca/FC.php?selectString=**&filter=both&sortOrder=natural&colorFlag=allFlag&colorStatus=allStatus&priority=importance-high&subsetFlag=miniQuiz&prefix=AAA&suffix=UncollReins§ion=all&subSection=all&examRep=all&examYear=all&examTerm=all&quizNum=6<span style="font-size: 20px; background-color: yellow; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 0px;">'''Multiple Choice (mini BattleQuiz 6)]'''</span> ← for general review of topic | ||

==Study Tips== | ==Study Tips== | ||

| Line 12: | Line 28: | ||

Something tells me this reading has a good chance of being tested because it's related to reinsurance, a heavily tested topic. The reading presents another method for estimating the "Uncollectible Reinsurance Reserve", or URR, and this is closely related to the calculation of the '''SAP''' ''[[Odomirok.14-F#Calculation:_Provision_for_Reinsurance | Reinsurance Provision]]'' which is the most heavily tested topic from ''[[Odomirok.14-F | Chapter 14 of Odomirok]]''. | Something tells me this reading has a good chance of being tested because it's related to reinsurance, a heavily tested topic. The reading presents another method for estimating the "Uncollectible Reinsurance Reserve", or URR, and this is closely related to the calculation of the '''SAP''' ''[[Odomirok.14-F#Calculation:_Provision_for_Reinsurance | Reinsurance Provision]]'' which is the most heavily tested topic from ''[[Odomirok.14-F | Chapter 14 of Odomirok]]''. | ||

| − | The estimation methods here are for '''GAAP''' financial statements and fortunately they are much simpler than the SAP reinsurance provision so you can learn them very quickly. There are a lot of other potential short-answer questions but | + | The estimation methods here are for '''GAAP''' financial statements and fortunately they are much simpler than the SAP reinsurance provision so you can learn them very quickly. There are a lot of other potential short-answer questions that fill in background information but are likely less important than the calculations. If you're running of out time to study before the exam, you can likely skip most of this reading and just focus on the methods and the basic concepts for each of the 2 methods for estimating URR. |

'''Estimated study time''': 1 day''(not including subsequent review time)'' | '''Estimated study time''': 1 day''(not including subsequent review time)'' | ||

| Line 36: | Line 52: | ||

[https://battleacts6us.ca/FC.php?selectString=**&filter=both&sortOrder=natural&colorFlag=allFlag&colorStatus=allStatus&priority=importance-high&subsetFlag=miniQuiz&prefix=AAA&suffix=UncollReins§ion=all&subSection=all&examRep=all&examYear=all&examTerm=all&quizNum=all<span style="font-size: 20px; background-color: lightgreen; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 10px;">'''Full BattleQuiz]'''</span> | [https://battleacts6us.ca/FC.php?selectString=**&filter=both&sortOrder=natural&colorFlag=allFlag&colorStatus=allStatus&priority=importance-high&subsetFlag=miniQuiz&prefix=AAA&suffix=UncollReins§ion=all&subSection=all&examRep=all&examYear=all&examTerm=all&quizNum=all<span style="font-size: 20px; background-color: lightgreen; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 10px;">'''Full BattleQuiz]'''</span> | ||

| − | [https:// | + | [https://battleacts.discourse.group/c/candidates-6u/aaa-uncoll-reins/193<span style="font-size: 12px; background-color: lightgrey; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 0px;">'''Forum'''</span>] |

==In Plain English!== | ==In Plain English!== | ||

| Line 147: | Line 163: | ||

{| class='wikitable' style='background-color: navajowhite; | {| class='wikitable' style='background-color: navajowhite; | ||

|- | |- | ||

| − | || The text further discusses concepts pertaining to the '''rating-based method''' by asking and answering several questions. I'm not sure how important these so I've abbreviated the answers given in the text. If you want more detail please refer to the source, but | + | || The text further discusses concepts pertaining to the '''rating-based method''' by asking and answering several questions. I'm not sure how important these are so I've abbreviated the answers given in the text. If you want more detail please refer to the source, but this will give you the main idea: |

|} | |} | ||

| Line 268: | Line 284: | ||

[https://battleacts6us.ca/FC.php?selectString=**&filter=both&sortOrder=natural&colorFlag=allFlag&colorStatus=allStatus&priority=importance-high&subsetFlag=miniQuiz&prefix=AAA&suffix=UncollReins§ion=all&subSection=all&examRep=all&examYear=all&examTerm=all&quizNum=all<span style="font-size: 20px; background-color: lightgreen; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 10px;">'''Full BattleQuiz]'''</span> | [https://battleacts6us.ca/FC.php?selectString=**&filter=both&sortOrder=natural&colorFlag=allFlag&colorStatus=allStatus&priority=importance-high&subsetFlag=miniQuiz&prefix=AAA&suffix=UncollReins§ion=all&subSection=all&examRep=all&examYear=all&examTerm=all&quizNum=all<span style="font-size: 20px; background-color: lightgreen; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 10px;">'''Full BattleQuiz]'''</span> | ||

| − | [https:// | + | [https://battleacts.discourse.group/c/candidates-6u/aaa-uncoll-reins/193<span style="font-size: 12px; background-color: lightgrey; border: solid; border-width: 1px; border-radius: 10px; padding: 2px 10px 2px 10px; margin: 0px;">'''Forum'''</span>] |

==POP QUIZ ANSWERS== | ==POP QUIZ ANSWERS== | ||

Latest revision as of 21:53, 26 January 2026

Reading: “Estimating the Uncollectible Reinsurance Reserve for Property/Casualty Companies New GAAP Requirements,” July 2019

- pp. 4-15.

Author: American Academy of Actuaries (AAA)

Forum (Or click here for Legacy Forum – no longer monitored)

VIDEO → (6:15) → Uncollectible Reinsurance - General Overview (Click here for all currently available videos.)

BA Quick-Summary: Estimating Uncollectible Reinsurance

|

Contents

Pop Quiz

Multiple Choice (mini BattleQuiz 6) ← for general review of topic

Study Tips

Something tells me this reading has a good chance of being tested because it's related to reinsurance, a heavily tested topic. The reading presents another method for estimating the "Uncollectible Reinsurance Reserve", or URR, and this is closely related to the calculation of the SAP Reinsurance Provision which is the most heavily tested topic from Chapter 14 of Odomirok.

The estimation methods here are for GAAP financial statements and fortunately they are much simpler than the SAP reinsurance provision so you can learn them very quickly. There are a lot of other potential short-answer questions that fill in background information but are likely less important than the calculations. If you're running of out time to study before the exam, you can likely skip most of this reading and just focus on the methods and the basic concepts for each of the 2 methods for estimating URR.

Estimated study time: 1 day(not including subsequent review time)

BattleTable

No past exam questions are available for this reading.

reference part (a) part (b) part (c) part (d)

In Plain English!

A new accounting requirement by FASB (ASU 2016-13) regarding uncollectible reinsurance reserves took effect in 2020 for certain filers of US GAAP statements and the following year for others. The new requirement establishes rules for determining uncollectible reinsurance reserves and introduces new disclosure requirements, potentially requiring changes in reserving practices for some insurers.

A working group by the Financial Reporting Committee of the American Academy of Actuaries wrote a white paper describing the new rules, discussing their impact on different companies, methods to estimate the reserves, and potential issues with U.S. Statutory accounting and Actuarial Standards of Practice.

Section 1 - What is the Issue?

Ceded reinsurance is a significant aspect of property/casualty companies' operations, and the collectability of ceded balances is crucial for solvency and risk evaluations. P&C companies maintain an uncollectible reinsurance reserve (URR) as a provision for reinsurance uncollectibility, which is recorded as an offset to their ceded reserve balances.

New rules issued by the Financial Accounting Standards Board (ASU 2016-13) in 2016 will bring changes to URR accounting for U.S. GAAP, effective from 2020 for public companies and 2021 for others.

Section 2 - What are the New Rules?

The recently introduced FASB regulations mandate a change in the way uncollectible reinsurance reserves are determined, specifically regarding credit risk. Under the new rules,

- these reserves must be established based on anticipated ultimate uncollectible amounts

This adjustment brings FASB more in line with other established standards like IFRS 17, Solvency II, and market-consistent methodologies used in Bermuda. Previously, insurers only considered known impairments when estimating their Uncollectible Reinsurance Reserves (URR), limited to reinsurers that were already recognized as impaired or financially weak as of the balance sheet date.

It is important to note that URR accounts for both credit risk and dispute risk. However, the FASB rules solely focus on the credit risk component, leaving the rules pertaining to the dispute risk portion of URR unchanged. Consequently, some companies might adopt an approach of using the anticipated ultimate uncollectible method for the credit risk portion of URR, while employing a known impairment method for the dispute risk portion. This discrepancy could result in differences between the accounting practices under the new FASB rules and those of IFRS 17 and Solvency II.

Section 3 - What is Current Practice?

In the current practice, companies generally employ a consistent approach when determining Uncollectible Reinsurance Reserves (URR) for both their U.S. GAAP and U.S. Statutory filings, although there may be variations across the industry. One approach is known as the incurred loss model where the URR estimate reflects only known impairments of reinsurers as of the balance sheet date. Another approach is the expected loss model where the URR estimate considers the ultimate uncollectible amount, including some provisions for reinsurers not yet impaired.

According to current accounting rules, U.S. GAAP supports either approach depending on the unit of account used in the valuation.

- If the unit of account is the balance with an individual reinsurer, a loss is recognized only if that reinsurer is impaired.

- If the unit of account is the total balance spread over multiple reinsurers, a company may determine that a loss is highly likely for at least some portion of the total balance.

- (Once a loss is deemed probable, financial statement preparers are required to provide their best estimate of that loss.)

The choice of the unit of account is an accounting policy decision, not an actuarial one, although actuaries may be involved in the measurement process.

U.S. Statutory accounting standards are generally based on U.S. GAAP standards issued by the FASB, allowing support for either approach. Additionally, U.S. Statutory requires the URR to be included in the loss reserve, with the added requirement that write-offs of previous ceded loss amounts be recorded in the same account as the initial ceded amount. Some argue that if the loss reserve is based on an ultimate valuation, the URR should follow the same basis (implying the use of the expected loss model). However, current practice appears to treat the URR in a similar manner for both U.S. GAAP and U.S. Statutory reporting.

Section 4 - Causes of Reinsurance Uncollectibility

This section is basically just a list of different causes for uncollectibility. So boring. I could see an exam question that asks you for the 2 main causes (credit risk, dispute risk) and the maybe asks you for a few specific examples of each.

The primary causes of uncollectibility are:

- credit risk (or inability to pay)

- dispute risk (or unwillingness to pay)

An inability to pay is generally due to either impairment or insolvency.

An unwillingness to pay could be due to differing interpretations of the reinsurance contract because of:

- unique exposures (alien invasion from Mars)

- rare events (a squirrel steals your sandwich)

- provisions untested in the courts (insurance against damages due to your future self traveling back in time to dump a bucket of water on your head)

- a circumstance not contemplated by the contract (the contract did not account for a Zombie Apocalypse)

But in all seriousness, reinsurance contract disputes have been common for latent liabilities, such as asbestos and environmental pollution. Some specific situations of where disputes can occur could be:

- missing policies (this could happen if the original contract is decades old)

- late notice of claim (that's a favorite way for insurers or reinsurers to deny claims)

- settlements made without first consulting with the reinsurer (if such a requirement is in the contract)

- definition of an "occurrence" (reinsurer may not accept that a covered event or occurrence actually happened, in the context of the contract)

The source text goes on to list several less obvious causes of uncollectibility risk, but I think the information above should be sufficient for the exam. If you want more information, please refer to the source text.

Section 5 - Estimation Methods

Definition of Insurance Write-off

This short section doesn't actually provide a definition of insurance write-offs. Rather, it merely highlights that different insurers may have different definitions (or methods) for accounting for write-offs in their system, so write-off histories for different insurers may not be directly comparable. Consequently, a method used by one insurer may not be appropriate for another insurer.

Two Methods

The 2 main methods for estimating URR are:

- rating-based method

- → uses financial strength ratings of reinsurers as the basis for a URR estimate

- → estimates credit-related URR only

- experience-based method

- → uses historical reinsurance write-offs as the basis for a URR estimate

- → estimates both credit-related URR and dispute-related URR

Rating-Based Method

Here we look at a simple example and then discuss some concepts pertaining to this method. (It's so simple that even Ian-the-Intern understands it!) Remember that the rating-based method uses financial strength ratings of insurers, so the given data of ceded billings and default rates are broken out by strength rating. In the text example, the strength ratings are labeled: A, B, C, D.

Note that the matrices of ceded billings and default rates by strength rating and by year are required for this method. Further down, the text discusses how a cumulative default matrix can be constructed from a transition matrix but does not provide an example, so you should only have to know the concept rather than the full calculation for that.

| Here's the problem... |

_problem.png)

| Here's the solution... |

_solution.png)

A variation on this problem could be to ask for the URR only for a specific year or a specific reinsurer rating. If so, make sure you provide this in your answer rather than giving only the total for all years and all reinsurers.

Notice how you're given a matrix of cumulative default rates and that they change over time. Since payouts of insurance liabilities may occur over many years, the probability of default may also change; an insurer may become stronger or weaker and the percentages in the matrix have to reflect that. (Note the potential situation where a reinsurer's rating changes, for example from D to C, so that they move to a different row in the tables above. This is discussed further down in the context of transition matrices.)

Excel Practice: URR - Rating-Based Method

| The text further discusses concepts pertaining to the rating-based method by asking and answering several questions. I'm not sure how important these are so I've abbreviated the answers given in the text. If you want more detail please refer to the source, but this will give you the main idea: |

Question: Does a reinsurer default imply that 100% of the associated reinsurance recoverable should be written off?

- no, some reinsurers may partially or fully recover and pay some or all amounts previously in default

- (or some funds may be recovered after insolvency resolution)

Question: When would you use incremental default rates rather than cumulative default rates?

- use incremental default rates when future ceded balances are projected on a runoff basis

- (cumulative default rates are applied to projected future reinsurance billings)

Question: How is the cumulative probability of default by rating estimated?

- A.M. Best Financial Strength Ratings and associated probability of impairment

- insurer’s history of reinsurer default rates by internal rating

- transition matrices (see below)

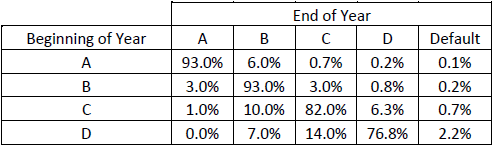

Question: How can transition matrices help insurers estimate cumulative default probabilities?

- an insurer without a long-term history of default ratios can use a transition matrix as in the example shown below

- → There is a 93% chance that an A-rated reinsurer will remain an A-rated reinsurer 1 year later

- → There is a 6% chance that an A-rated reinsurer will become a B-rated reinsurer 1 year later

- → There is a 0.7% chance that an A-rated reinsurer will become a C-rated reinsurer 1 year later

- → There is a 0.2% chance that an A-rated reinsurer will become a D-rated reinsurer 1 year later

- → The last column shows the one-year cumulative default probability

- use this matrix to create a new distribution of reinsurers by financial strength rating at the beginning of year 2

- repeat for all years

- Result: a table of cumulative default probabilities over the lifetime of the expected reinsurance billings

_transition_matrix.png)

Question: How is the URR provision for disputes treated in a rating-based method?

- calculate dispute provision by considering any or all of:

- → insurer’s prior dispute-based reinsurance write-offs

- → industry data to the extent available and relevant

- → management’s judgment

Question: How can double-counting be avoided when estimating URR?

- apply the URR rating-based method to the reinsurance recoverable net of the calculated dispute provision

Experience-Based Method

Here we look at another simple example, this time for the experience-based URR method, and then discuss some concepts pertaining to this method. (It's so simple that even Ian-the-Intern's little brother understands it!) Recall that this method uses an insurer's historical reinsurance write-offs as the basis for a URR estimate.

| Here's the problem... |

_problem.png)

| Here's the solution... |

_solution.png)

Excel Practice: URR - Experience-Based Method

| Similar to the previous section on the rating-based method, the text further discusses concepts pertaining to the experience-based method. |

| Question: How is the experience-based method applied in practice? |

- simplest: combine multiple years (as shown above) to overcome the impact of write-off delays and year-by-year variation

- enhancements: incorporate such elements as:

- → write-offs over time by billing lag year (allows for reinsurer deterioration)

- → reinsurance structure (quota share, per-occurrence excess of loss, aggregate excess of loss)

- → line of business

Question: What are the challenges associated with experience-based URR methods?

- thin data (an insurer may have little or no historical reinsurance write-offs)

- past uncollectible rates may not be indicative of future uncollectible rates (this is true for any predictive modeling)

- experience-based uncollectible rates can be distorted by individual events (commutations, reinsurer insolvency)

- and several more are listed in the source text...

Question: When is it appropriate for an insurer to use experience-based methods?

- when their write-off experience has sufficient credibility

- (otherwise consider a rating-based method)